Established in 1932 by the Federal Home Loan Bank Act, the FHLBank System consists of 11 regional FHLBanks, each serving a designated geographic area of the United States and its territories, and the Office of Finance.

Each FHLBank is a separate, government-chartered, member-owned corporation that provides its members with funding for mortgages and asset-liability management, liquidity for short-term needs, and additional funds for housing finance and community development.

The FHLBanks provide liquidity to members mainly through advances, which are long- and short-term loans priced at a small spread over comparable U.S. Department of the Treasury obligations. Advances are primarily collateralized by residential mortgage loans, and government and agency securities. Community financial institutions also may pledge small business, small farm, and small agri-business loans as collateral for advances. View FHFA’s Report on Collateral Pledged to FHLBanks.

The FHLBanks also offer Acquired Member Asset programs, through which they purchase residential mortgages from their members, and support affordable housing and community development through programs including the Affordable Housing Program, the Community Investment Program, the Community Investment Cash Advance Program, and various FHLBank voluntary programs.

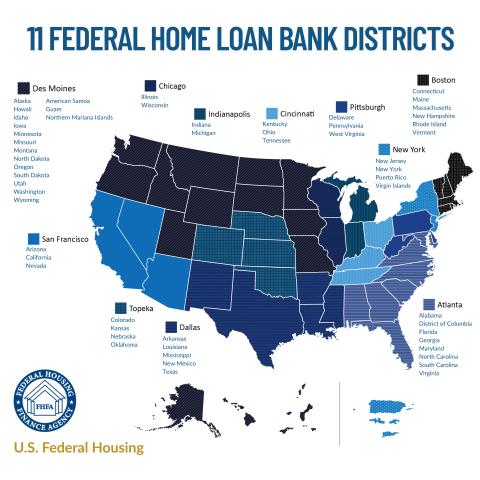

Regional FHLBanks are located in Atlanta, Boston, Chicago, Cincinnati, Dallas, Des Moines, Indianapolis, New York, Pittsburgh, San Francisco, and Topeka. See FHLBank Districts for more information about FHLBank locations and districts.

- Review Advisory Bulletins issued by FHFA for the FHLBank System

- See the Code of Federal Regulations: FHLBanks

- Learn more about the Rulemaking process

- See FHLBank stress tests and market risk scenarios

- See FHFA’s Affordable Housing and Community Investment home page

View PDF version of 11 Federal Home Loan Bank Districts map.

FHLBank Membership

FHLBank members include commercial banks, thrifts, credit unions, community development financial institutions (CDFIs), and insurance companies.

Eligible financial institutions join the FHLBank district that serves the state where the institution's home office or principal place of business is located. A financial institution may become a member by meeting requirements provided in 12 USC 1424:

- be duly organized under the laws of any state of the United States;

- be subject to inspection and regulation under the banking laws, or similar state or federal laws;

- make long-term home mortgage loans;

- have at least 10 percent of its total assets in residential mortgage loans, if it is a federally insured depository institution (community financial institutions are exempt from this requirement);

- have a financial condition that allows FHLBank advances (loans) to be made safely;

- have character of management and a home financing policy consistent with sound and economical home financing.

Each member of the FHLBank must maintain a minimum investment in the stock of the FHLBank, established by the FHLBank, and the sum of the stock investment by all members must be sufficient for the FHLBank to meet its own minimum capital requirement. Contact the FHLBank for more information concerning minimum stock requirement.

- See FHFA regulation 12 CFR 1263 governing FHLBank membership.

- See FHLBank Membership Data for more information about FHLBank members.

FHLBank Funding

While the FHLBanks' mandate reflects a public purpose, they are privately capitalized and receive no appropriated federal funds.

The FHLBanks fund themselves principally by issuing consolidated obligations, which consist of bonds and discount notes (which have an original maturity of less than one year and are sold at a discount). The Office of Finance acts as the FHLBanks’ agent and offers, issues, and services consolidated obligations of the System in the public capital markets.

Consolidated obligations are not guaranteed or insured by the federal government. However, the FHLBanks’ status as a government-sponsored enterprise accords certain privileges and enables the FHLBanks to raise funds at rates slightly above comparable obligations issued by the U.S. Department of the Treasury.

Although each FHLBank is a separate corporate entity with its own management and board of directors, the FHLBanks are jointly and severally liable for all System consolidated obligation debt.

Visit the Office of Finance website for more information on debt issuance and other System financial data.

FHLBank Directors

The FHLBanks are governed by boards of directors ranging in size from 9 to 22 directors, all of whom are elected by member institutions. Most FHLBank board members are directors or officers of member institutions, while the remaining directors (at least 40 percent) are independent. Independent directors are those who are not officers of an FHLBank or directors, officers, or employees of a member institution.

Learn more about FHLBank director compensation.

Director Applications

- Download a fillable Independent Director Application form.

- Download a fillable Independent Director Annual Certification form.

- Download a fillable Member Director Eligibility Certification form.

- Download the reference guide, Locking Fillable PDF Field to Read Only, for instructions on how to lock the information FHLBanks complete on the first page of each form.